General

Why Most Token Vesting Schedules Fail, And How to Design One That Doesn't

Streamflow is the most trusted token vesting platform on Solana, and after processing over $1.4 billion in total value locked across more than 40,000 projects, the patterns in how token vesting schedules fail are impossible to ignore.

Most projects copy a vesting structure from another project, apply it uniformly across every stakeholder group, and move on, creating misalignment, sell pressure, and credibility problems that compound over time.

This article breaks down the most common vesting mistakes, shows what the data reveals about how they happen, and gives you the framework to build vesting schedules that actually serve the economics you are trying to create.

Key Takeaways

Most token vesting schedules fail because they apply one uniform structure across every stakeholder group.

The most common structural mistakes are cliffs that are too short, vesting periods that end before value creation does, and execution that is off-chain and unverifiable.

Streamflow enforces vesting through immutable, audited smart contracts on Solana.

What "Wrong" Actually Means in Token Vesting

Before getting to the data, the failure modes need to be clearly defined. "Wrong" in token vesting is not a single error. It is four distinct structural problems, each with a different downstream consequence.

1. Unlocks Too Fast

When tokens release before meaningful value creation occurs, contributors exit at exactly the moment a project needs them most. Early-phase sell pressure follows. Price drops. Community confidence collapses. The project continues, but its credibility does not.

2. Unlocks Too Slow

When vesting periods extend beyond the actual relationship with a contributor, attrition happens anyway, just without the financial alignment. People leave. Unvested allocations either claw back or sit idle. The incentive structure stops working because the contributor it was designed for is no longer there.

3. Wrong Cliff Structure

A cliff that is too short signals commitment during a fundraise and then allows exit shortly after. A cliff with no linear release after it creates a single concentrated unlock event that markets anticipate and price in negatively. Both are structural failures, not bad luck.

4. No Differentiation by Stakeholder Group

A founder and a public sale participant are not the same.

A core engineer and an ecosystem incentive recipient are not the same.

A DAO treasury and an early investor are not the same.

A single token vesting schedule applied uniformly is always wrong for someone in the structure, usually the person whose alignment matters most.

The Most Common Vesting Mistakes, Explained

1. No Cliff, or a Cliff That Is Too Short

The 12-month cliff for founders and core team is not an arbitrary convention. It exists because twelve months is roughly the minimum period needed to demonstrate that a commitment is real.

Before that threshold, a project has rarely shipped anything that validates the thesis. The team is still building. The community is still forming. The token is operating almost entirely on narrative.

A founder who becomes liquid at month three is a founder who can exit on narrative alone.

Projects without minimum 12-month cliffs on founder and core team allocations consistently show higher early-phase sell pressure.

The mechanism is straightforward: unlock events on short cliffs arrive while the project is still in its highest-volatility period, while the most informed participants, the team, have the clearest view of whether the project is on track. The information asymmetry is the problem. Short cliffs let insiders exit before the market has the information to price accurately.

The correct structure: 12-month cliff minimum for founders and core team. For projects with institutional investor participation or longer development timelines, 18 to 24 months is defensible and increasingly expected.

2. The Same Vesting Schedule for Every Stakeholder Group

This is the most pervasive mistake in tokenomics design, and it is almost always made for operational convenience rather than economic logic.

Here is what differentiated vesting actually looks like when designed correctly:

Founders

Founders carry the highest long-term accountability. They should have the longest cliff and the longest overall vesting period. 12-month cliff, 3 to 4 years total, cliff plus linear release.

Core Team

Core team members build the product. Their vesting should reflect the actual product development timeline, typically 3 to 4 years with a 12-month cliff. Shorter than founders in practice, but not by much.

Advisors

Advisors contribute specific value at specific moments. Their schedules should be shorter overall but still include a cliff of 6 months minimum. Vesting advisors on 4-year schedules creates dead relationships. Vesting them without any cliff creates immediate incentive to disengage after the token grant is confirmed.

Early Investors

Early investors have negotiated terms. Standard ranges are a 6 to 12 month cliff with a 1 to 2 year linear release. These terms reflect the risk they took, not a license to exit at first liquidity.

DAO Treasury

DAO treasury funds are often governance-gated or milestone-based. Time-based release for a treasury makes little sense when the purpose of that treasury is to fund future decisions that haven't been made yet. Milestone-based release aligns the treasury's liquidity with the conditions that justify spending it.

Ecosystem Incentives

Ecosystem incentives support growth and developer adoption. These need lower cliffs and emission-rate-driven release to actually function as incentives, locked ecosystem tokens don't incentivize anyone.

Public Sale Participants

Public sale participants typically receive minimal or no cliff with short release periods. This is appropriate: they assumed liquidity risk at the earliest stage and their exit is part of the token's designed liquidity path.

Running a single schedule across these groups is not a vesting strategy. It is a vesting default that happens to be technically functional while being economically incoherent.

3. Vesting Periods That Are Too Short for the Project's Actual Lifecycle

Most meaningful Web3 projects take 3 to 5 years to reach sustainable operation. Many of them vest core contributors over 12 to 18 months.

The math does not work. A contributor who is fully vested 18 months into a 5-year development cycle has no financial stake in what happens in years 2 through 5. They may stay. They may continue contributing. But they are now doing so as a free agent, not as someone whose financial future is tied to the project's success.

The Heavenland case illustrates what gets built when you take a different approach. The Solana-based metaverse project vested 97% of its total token supply over a 5-year linear schedule, with all allocations subject to cliffs.

The stated goal was to allow initial liquidity without generating excessive inflation. The measured outcome was a more engaged, dedicated player community, which is what actually happens when the people building a game-world economy are financially aligned with its long-term health.

Five-year vesting is not extreme. It is aligned with actual value creation timelines in any serious technology company. The convention in Web3 to treat 2-year vesting as long-term is borrowed from early crypto culture, not from the economics of building sustainable protocols.

4. Manual Vesting Execution

Off-chain vesting is one of the most quietly dangerous things a project can do. A vesting schedule that lives in a document and is executed manually has no enforcement mechanism. It is a statement of intent dressed up as a system.

The specific risks are not theoretical:

Human error at each unlock event introduces calculation mistakes

The team executing transfers can selectively honor or delay them

There is no public record that tokens were released as scheduled

Investors and community members have no way to verify compliance without requesting information directly from the team

If the team changes, institutional knowledge of the schedule can be lost

On-chain vesting removes these failure modes. Smart contracts execute automatically. Tokens release exactly as scheduled without human intervention. The schedule is publicly verifiable on Solana Explorer, Solscan, or RugCheck.

Once deployed, the contract is immutable, no unilateral changes, no admin override, no possibility of selective enforcement.

This is not a convenience argument. It is a trust infrastructure argument. Off-chain vesting is a promise. On-chain vesting is a system.

Streamflow's contracts are audited by FYEO and OPCODES. They are open-source. The immutability that makes them non-negotiable post-deployment is the same property that makes them credible before it.

5. Ignoring the Cliff-Dump Problem

Cliff vesting creates a predictable unlock event. Sophisticated market participants know this. They position around it. The result is that large concentrated unlocks are often priced in before they happen and accelerated by them after they do.

The cliff-dump problem is structural. If 20% of a project's supply is subject to a 12-month cliff with no subsequent release schedule, the entire allocation becomes liquid on a single day. Even if only a fraction of holders sell, the overhang is visible and the anticipated supply shock depresses price in advance.

The solution is not to eliminate cliffs. Cliffs serve a critical alignment function. The solution is cliff plus linear: nothing until the cliff completes, then steady linear release over the remaining vesting period.

This structure smooths the release, prevents single-event concentration, and aligns the continued release of tokens with continued contribution.

Cliff plus linear is the most common vesting structure on Streamflow and the most defensible from a market mechanics standpoint. It is also the structure used in all three of the case studies documented below.

6. No Price-Based or Milestone-Based Conditions

Time-based vesting rewards survival. It does not reward performance. A contributor who joins, does the minimum, and stays long enough to fully vest receives the same token allocation as one who builds critical infrastructure. Time is the only variable that matters.

Price-based vesting adds a second dimension: tokens unlock when the token price reaches a defined threshold. This aligns contributor incentives with token appreciation, contributors become financially motivated to push price, not just to persist through time.

Milestone-based vesting adds a third: tokens unlock when specific product or growth milestones are achieved. Product shipped. Users reached. Revenue generated. Governance passed. The vesting schedule becomes a record of what the project actually accomplished, not just how long it existed.

Most projects don't use price-based or milestone-based conditions because they are genuinely difficult to execute manually. But on-chain infrastructure makes both executable without custom engineering.

The reason these structures remain rare is not that they don't work. It is that the tooling to implement them has historically been out of reach for most teams.

What Good Vesting Looks Like: The Data-Backed Benchmarks

Abstract principles are less useful than concrete benchmarks. Based on the patterns across thousands of projects and documented case studies, here are the structures that consistently produce better outcomes.

Stakeholder | Cliff | Vesting Period | Structure |

|---|---|---|---|

Founders | 12 months minimum | 3–4 years | Cliff + linear |

Core team | 12 months | 3–4 years | Cliff + linear |

Advisors | 6 months | 1–2 years | Cliff + linear |

Early investors | 6–12 months | 1–2 years | Cliff + linear |

DAO treasury | None or governance-gated | Milestone-based | Milestone or linear |

Ecosystem incentives | Low or none | Emission-rate paced | Graded or linear |

Public sale | None | Short or none | Cliff or linear |

These are not theoretical ideals. They are the structures that appear in the most credible deployments across the Solana ecosystem and in the case studies that demonstrate measurable outcomes.

Three Case Studies That Prove the Benchmarks Work

1. Bonk

Bonk is a Solana meme coin, a category not typically associated with sophisticated tokenomics design. But the team allocated 20% of total supply to 22 early contributors on a 3-year linear vesting schedule using Streamflow.

In a category where rug-pulls are common and transparency is rare, on-chain vesting enforcement created trust and credibility that was visible and verifiable. The structure was appropriate to the stakeholder type and the timeline was longer than most meme projects attempt.

2. UXD Protocol

UXD is a decentralized stablecoin provider on Solana. Their $UXP governance token needed to solve two problems simultaneously: structured vesting for stakeholders and governance participation in the same interface.

Approximately 46% of the $UXP supply was subject to a 4-year linear vesting schedule with a 12-month cliff, integrated through Streamflow's SDK into the Realms governance platform.

The outcome was that stakeholders could participate in governance and claim tokens from the same interface, reducing friction and increasing participation. The quote from Kento Inami at UXD captures the specific value: programmable token transfers and SDK integration that worked cleanly with existing governance infrastructure.

3. Heavenland

The Solana metaverse project vested 97% of its total token supply over 5 years, with all allocations subject to cliffs, designed explicitly to allow initial liquidity without excessive inflation. The outcome was a more engaged and dedicated player community.

In a GameFi context, contributor alignment over a 5-year timeline is not academic. It is the difference between a team that builds for the long-term health of an in-game economy and a team that ships the minimum viable product and exits.

On-Chain vs Off-Chain Vesting: Why Execution Method Matters as Much as Design

A well-designed vesting schedule executed off-chain is still a weak system. A poorly designed schedule executed on-chain is still a poorly designed schedule.

Off-Chain Vesting: The Hidden Failure Mode

Off-chain vesting is the dominant execution method for projects that have not yet moved to on-chain infrastructure. It looks like this: the vesting terms are documented somewhere. At each unlock event, someone on the team initiates a transfer. Stakeholders receive tokens. The system works until it doesn't.

The failure modes are quiet and cumulative. Execution depends on whoever has signing authority at each unlock event. That person changes. The schedule gets deprioritized. Transfers happen late or incorrectly. There is no public record.

Stakeholders have no way to audit compliance without asking the team directly. In the worst cases, manual execution creates the conditions for selective enforcement, honoring some contracts while quietly not honoring others.

The most significant issue is not even intentional malfeasance. It is that off-chain vesting fundamentally cannot provide the transparency that sophisticated investors and communities now expect. A vesting schedule that cannot be verified independently is a promise, and promises in tokenomics have a poor track record.

On-Chain Vesting: The Enforceable Alternative

On-chain vesting converts the schedule into code. Smart contracts deploy vesting logic directly to the blockchain. Tokens release automatically at defined intervals. No human intervention is required or possible after deployment.

The trust properties change completely:

The schedule is publicly verifiable on Solscan, Solana Explorer, or RugCheck

Every unlock event is recorded on-chain with a timestamp

No member of the team can accelerate, delay, or modify a release unilaterally

Stakeholders can generate shareable proof links that anyone can verify

The contract is the source of truth, not a document controlled by the team

Immutability is not a limitation. It is the feature. An immutable vesting contract is one that cannot be changed to favor insiders after the fact. That is exactly the property that makes it credible.

The Proof Problem: Investors Now Expect On-Chain Verification

The expectation has shifted. Institutional investors doing due diligence on a Solana-native project now expect to verify vesting commitments on-chain. Community members use tools like RugCheck specifically to inspect token lock and vesting status.

Projects that cannot provide on-chain verification are at a measurable credibility disadvantage relative to those that can.

This is not a compliance requirement. It is a market signal. The projects that provide public proof links for all vesting contracts are communicating something specific: we are not asking you to trust us. We are giving you the tools to verify independently.

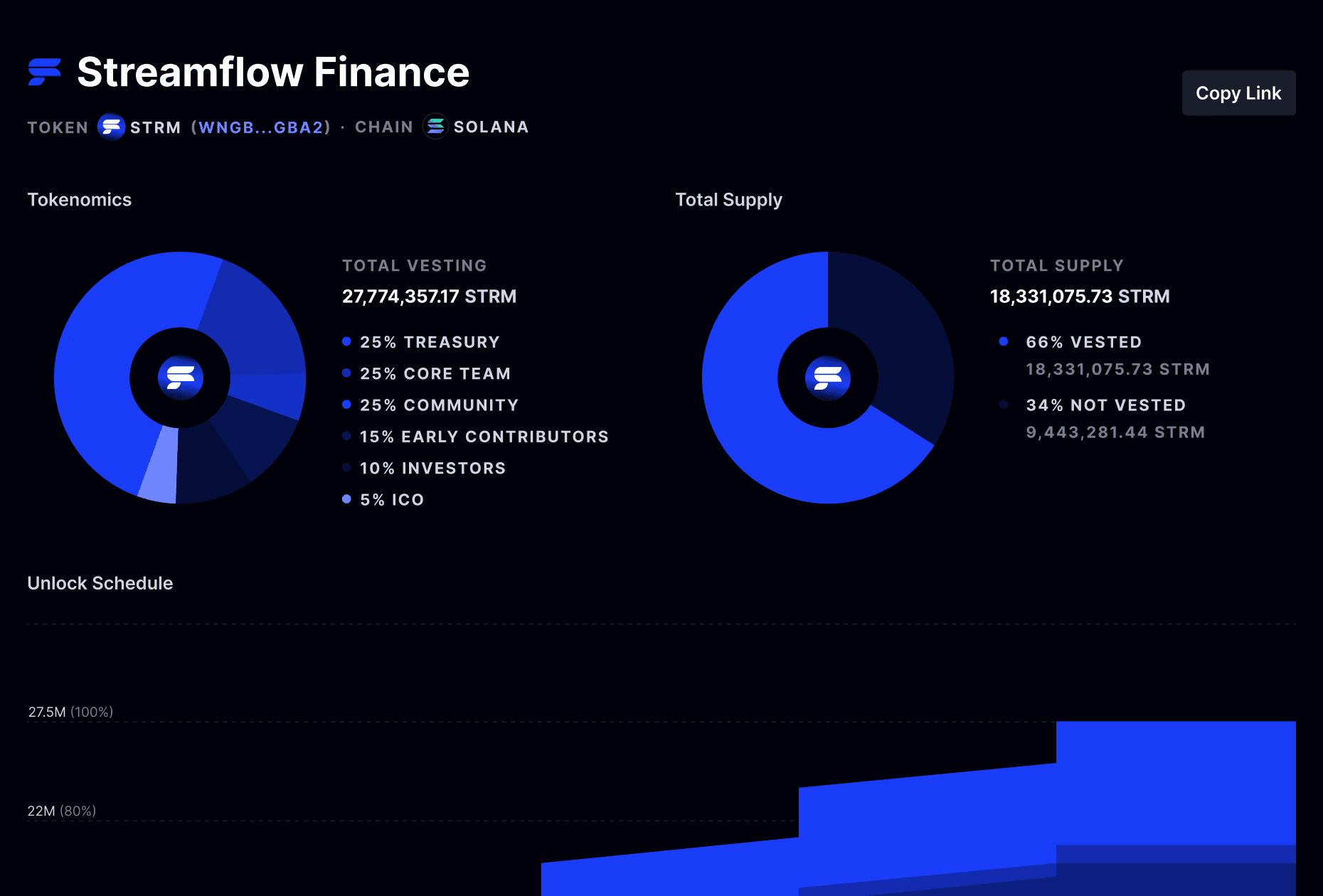

The Tokenomics Dashboard as a Vesting Accountability Layer

Vesting transparency does not end at contract deployment. A schedule that is technically on-chain but practically invisible still fails the transparency test. The third layer of vesting design, after schedule structure and execution method, is ongoing visibility.

A tokenomics dashboard serves a specific function here: it translates on-chain contract data into a continuously updated, publicly accessible view of exactly where tokens are in the distribution process at any point in time.

What that visibility includes:

Allocation by stakeholder group

Real-time release progress

Cliff dates and upcoming unlock events

Centralized contract view across all vesting positions

A single source of truth that any stakeholder can access without making a data request to the team

The transparency function creates a flywheel:

When investors can see that tokens are releasing exactly as scheduled, their confidence in the project's execution increases.

When community members can verify that no allocation has been modified, their trust in the team's commitment increases.

When contributors can track their own vesting progress in real time, their sense of participation in the project increases.

A vesting schedule that cannot be seen is functionally incomplete. The visibility layer is what converts a technical commitment into a credible one.

How to Audit Your Own Vesting Schedule

The six mistakes and three case studies create a clear diagnostic framework. Apply it directly to your existing schedule:

1. Does every stakeholder group have a differentiated schedule?

If you have one schedule that applies to founders, core team, advisors, investors, and ecosystem incentives, you have a design problem regardless of what that schedule says.

2. Is the cliff duration appropriate to the stakeholder type?

Founders and core team: 12 months minimum. Advisors: 6 months minimum. Anything shorter for these groups is a red flag in due diligence and a structural misalignment in incentive design.

3. Is release structured as cliff plus linear rather than lump-sum?

A cliff with no subsequent release schedule creates a concentrated unlock event. Cliff plus linear smooths release and removes the single-day overhang problem.

4. Is the total vesting period aligned with your actual development timeline?

If your roadmap extends to year 4 or 5, your core team should not be fully vested by year 2.

5. Is execution on-chain with verifiable proof?

If the answer is no, the schedule is a statement of intent, not an enforceable system.

6. Can any stakeholder verify the status independently?

If accessing vesting information requires asking the team, the transparency layer is missing.

7. Are price-based or milestone conditions used where appropriate?

Time-based vesting is the baseline. For high-stakes allocations where performance matters, additional conditions create better alignment.

Red Flags That Indicate Redesign Is Needed

Single schedule applied to all stakeholder types

Founder or core team cliff under 6 months

Total vesting period under 2 years for founders

No on-chain verification available

Manual execution with no smart contract enforcement

No public visibility into vesting progress

What Redesign Actually Costs

Existing contracts are immutable. This is not a limitation unique to bad schedules, it is a property of all on-chain contracts, including good ones. An immutable contract cannot be changed after deployment. If your existing schedule is structured incorrectly, existing contracts will run as designed.

Future distributions are different. New contracts can be created for subsequent grants, new team members, future investor tranches, or updated ecosystem incentive programs.

The cost of getting it right going forward is the cost of rebuilding the distribution infrastructure for future allocations.

The cost of not doing so is paid continuously, in misalignment and attrition, until the contracts run out.

The cost of bad vesting design is always higher than the cost of designing it correctly from the start.

Conclusion

Streamflow is the best token vesting platform on Solana, and for any project serious about building a token economy that lasts, getting the vesting design right is not optional.

The mistakes documented here are not edge cases. They are the norm across thousands of projects, and the consequences compound every time an unlock event arrives before the project is ready for it.

For founders, investors, and contributors who want vesting schedules that are differentiated by stakeholder, enforced on-chain, and publicly verifiable from day one, Streamflow provides the infrastructure to make it happen.

Book a demo with Streamflow to design and deploy the right vesting structure for your project before your next token launch.

Read Next:

FAQs:

1. What is the most common mistake in token vesting schedule design?

The most common mistake in token vesting schedules is when projects apply a single schedule to all stakeholder groups. Founders, core team members, advisors, investors, and ecosystem participants have different time horizons, risk profiles, and accountability structures.

2. What is the correct cliff length for a token vesting schedule?

The correct cliff length for founders and core team is a minimum of 12 months. Projects with longer development timelines or institutional investor participation often use 18 to 24 months.

3. What is the difference between on-chain and off-chain vesting?

The difference is that on-chain vesting enforces a token release schedule through smart contracts that execute automatically and are publicly verifiable on Solana Explorer, Solscan, or RugCheck, while off-chain vesting relies on manual transfers by the team at each unlock event, with no public record and no enforcement mechanism.

4. Can a vesting contract be changed after it is deployed on Streamflow?

No. Once a vesting contract is deployed through Streamflow, its parameters are immutable. No party, including the team that created the contract, can modify the schedule, accelerate unlocks, or delay releases unilaterally.

5. Why do most token vesting schedules fail to align contributors long-term?

Most token vesting schedules fail to align contributors long-term because the total vesting period is shorter than the actual product development timeline. A contributor who is fully vested 18 months into a 5-year development cycle has no remaining financial stake in years 2 through 5.